Climate physical risk is now sitting in African agri loan books

The 2022 drought across the Horn of Africa drove non-performing loans in agricultural portfolios up by 200 to 400 basis points across multiple Tier 2 lenders we have worked with. The 2024 East African floods did similar damage, in different counties, to different crops, in the same loan books. This is not a once-a-decade tail event any more. It is the new climatology.

Physical climate risk is now sitting inside African agricultural loan books as a measurable, recurring driver of expected credit loss. Few banks have measured it. Most still treat agri losses as idiosyncratic borrower events rather than climate-driven portfolio events.

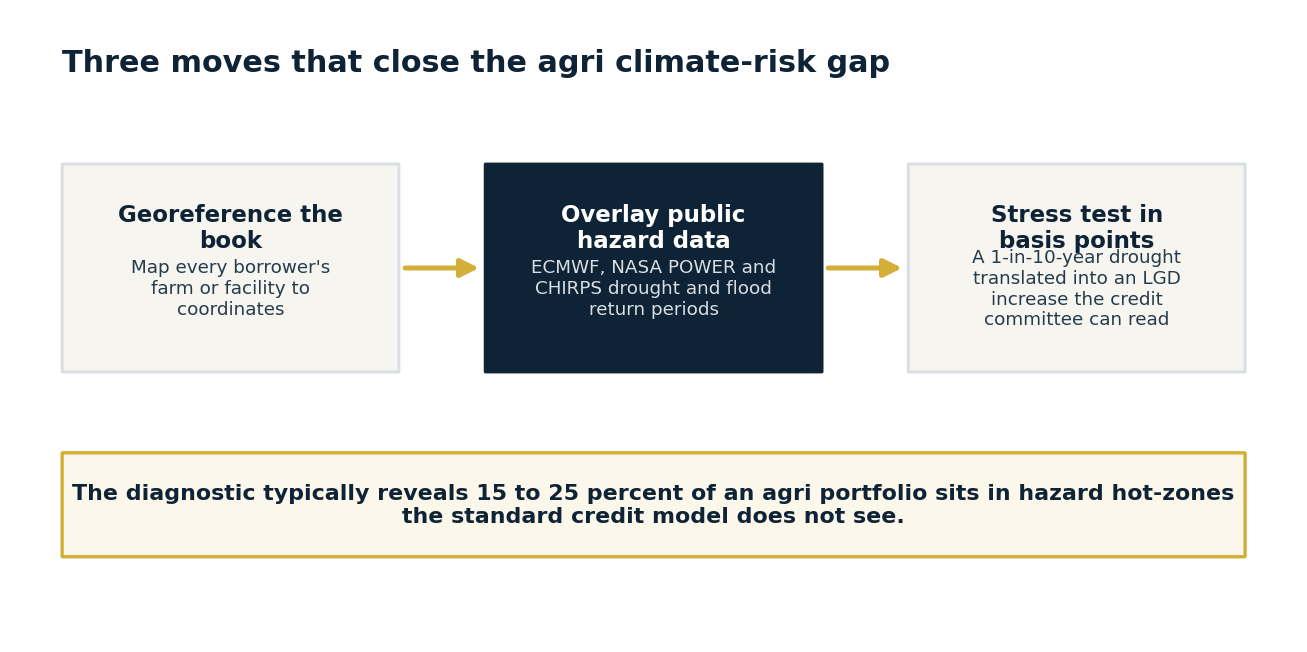

Three moves that close the gap

Three concrete moves close the gap, and none of them is glamorous.

- Georeference the agri loan book. If you do not know what coordinates your borrowers' farms or processing facilities sit on, you cannot overlay drought, flood, or temperature-anomaly data on them. The first deliverable on every agri-portfolio climate engagement is a georeferenced borrower map. Many banks resist this on data-privacy grounds; the regulatory pressure in 2026 is moving sharply in favour of doing it anyway.

- Build a hazard overlay using public climate data. ECMWF, NASA POWER, and CHIRPS rainfall datasets are free, well-documented, and have historical depth going back decades. Sub-county-level drought and flood return periods can be built from them. The output is a hazard score per borrower location that you can join to LGD assumptions in your ECL model.

- Stress test, do not narrate. A 1-in-10-year drought scenario applied to the georeferenced book should produce a portfolio-level impact you can report to the credit committee in basis points of LGD increase. If your scenario output is a narrative paragraph rather than a number, you do not have a stress test. You have a memo.

The diagnostic typically reveals that 15 to 25 percent of an agri portfolio sits in hazard hot-zones that the bank's standard credit model does not see. That is the provisioning conversation worth having.

Where ARMA comes in

ARMA's agri climate stress engagement is a 10 to 14 week build that delivers a georeferenced loan book, a public-data hazard overlay, and a credit-committee-ready scenario output. It is built for Tier 2 and Tier 3 African banks with material agricultural exposure, typically 15 to 35 percent of the book. Visit client.africarisk.net to scope the engagement.