Why credit providers need to keep raising their credit skills [2018]

Originally published April 2018, republished here as part of ARMA's continuity record. The argument has only become more urgent.

A few years ago, ARMA worked with FSD Africa and IPC GmbH on a continent-wide credit-skills assessment. The headline finding was simple and uncomfortable: most African credit officers had been trained for a credit environment that no longer exists, by trainers using curricula that had not kept pace with regulatory, climate, or digital realities.

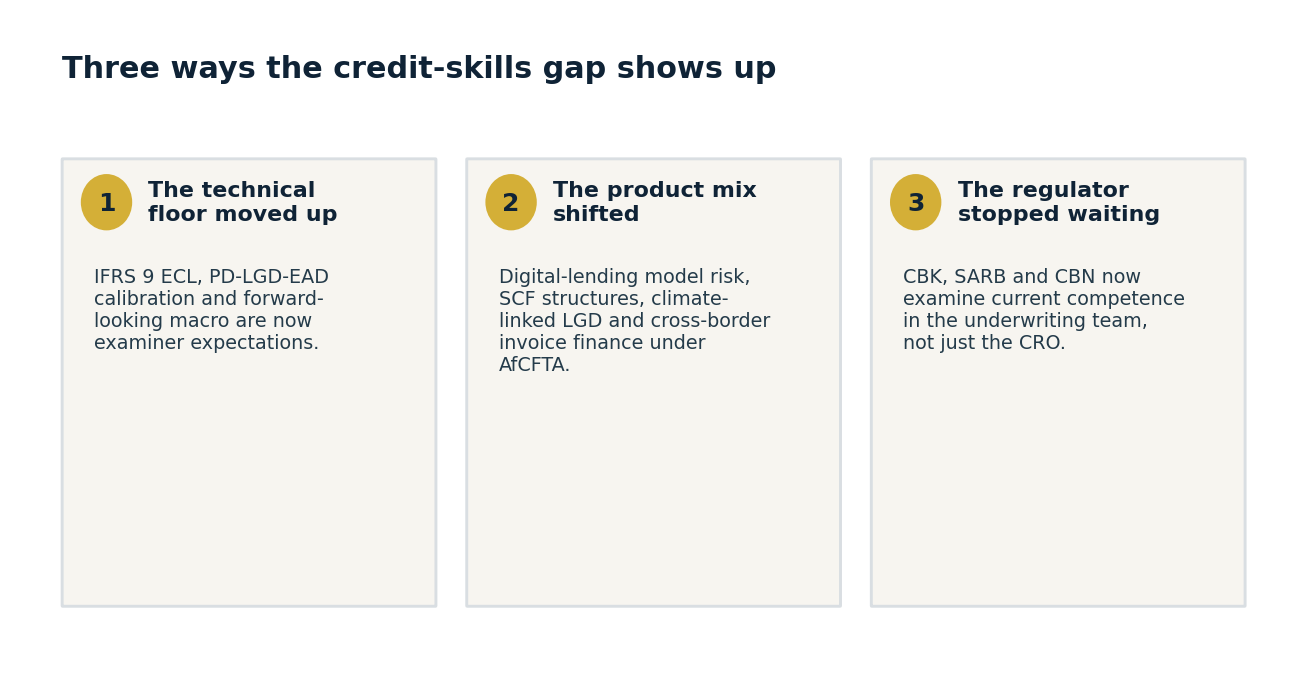

Three ways the gap shows up

The gap shows up in three ways.

- The technical floor has moved up. IFRS 9 implementation across African banks raised the bar on credit risk modelling. ECL methodology, PD-LGD-EAD calibration, and forward-looking macroeconomic adjustments are now examiner expectations, not aspirations. Credit officers trained pre-2018 often inherited frameworks they did not build and cannot explain. This is dangerous.

- The product mix has shifted. Five years ago, a competent SME credit officer needed strong cash-flow analysis and collateral valuation skills. Today they additionally need to understand digital lending model risk, supply chain finance structures, climate-linked LGD adjustments for agri exposures, and cross-border invoice finance under AfCFTA. The job description has expanded; many training programmes have not.

- The regulator is no longer accepting on-the-job learning as a substitute. Central Bank of Kenya, SARB, and CBN have all elevated supervisory expectations on credit risk management competence, not just at the CRO level but in the credit underwriting team. Pillar II reviews now examine whether the people approving loans have demonstrably current skills.

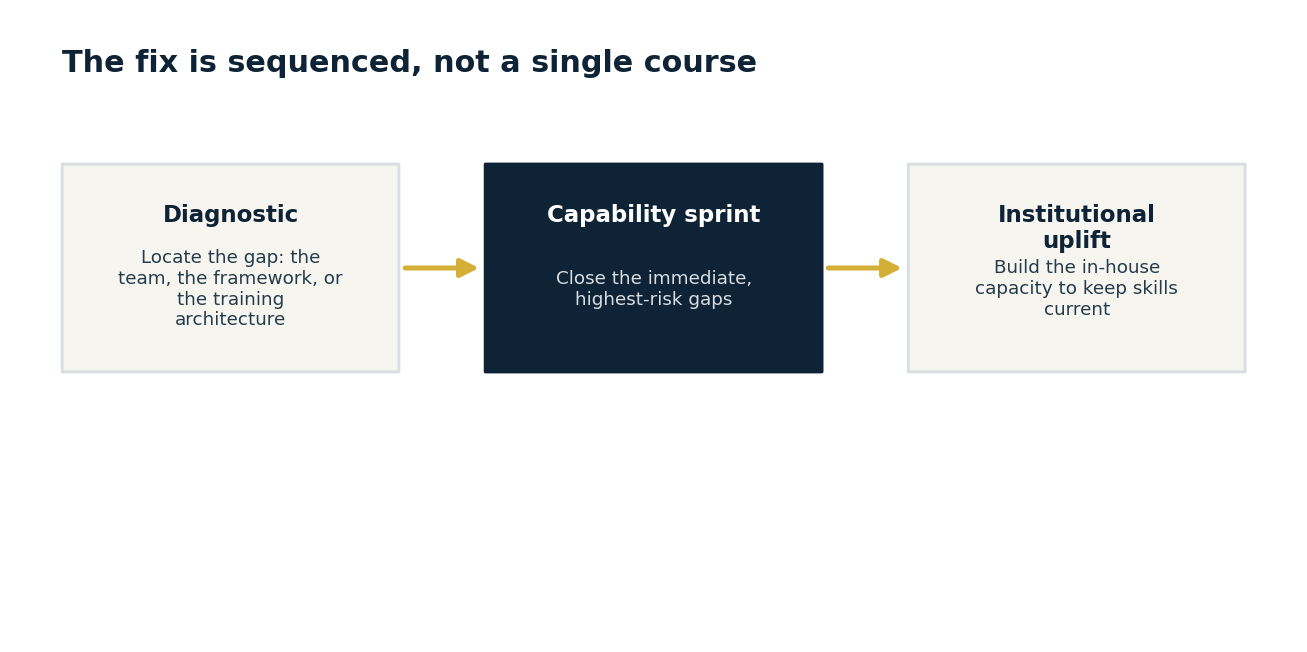

The fix is sequenced

The fix is sequenced. A credit-skills diagnostic identifies where the gap actually sits: sometimes in the team, sometimes in the framework, sometimes in the training architecture itself. A short capability sprint addresses the immediate gaps. A longer institutional uplift builds the in-house capacity to keep skills current as the operating environment continues to evolve.

What has changed is that the gap is now larger, the regulator is less patient, and the cost of getting it wrong shows up in NPL ratios and supervisory findings within 12 months, not over a decade.

Where ARMA comes in

ARMA's credit-skills engagement is a 6 to 10 week diagnostic plus capability sprint that delivers a team competency gap analysis, a refreshed credit underwriting framework where required, and a CPD-accredited training programme keyed to your portfolio. It is built for Tier 2 and Tier 3 African banks, NBFIs, and SACCOs with material credit growth ambitions. Visit client.africarisk.net to scope the engagement.