Supply chain finance as a financial inclusion tool

The conventional financial inclusion playbook in Africa has been mobile money plus microfinance. Both have done remarkable work. Both have run into the same ceiling: they extend transactional access without extending working capital that scales with the business. The SME that needs $40,000 to fulfil a confirmed buyer purchase order is not going to get there on M-Pesa overdraft and a $3,000 unsecured microloan.

The inclusion lever the development community has under-deployed

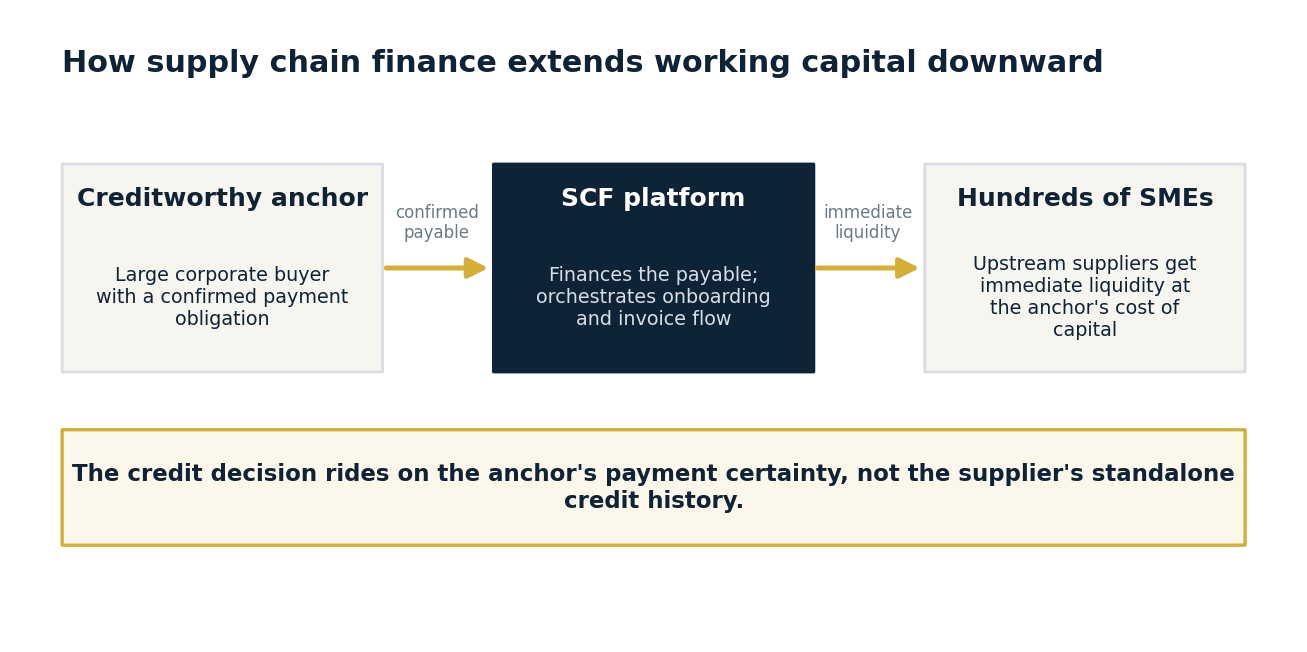

Supply chain finance is the financial inclusion lever that the development finance community has under-deployed in Africa. Done well, it converts an anchor corporate's payment terms into immediate liquidity for hundreds of upstream SMEs, with the credit decision keyed off the anchor's payment certainty rather than the SME's stand-alone risk profile. This is the right structure for African informal-economy suppliers because it does not require them to have audited financials or three years of operating history.

Three structural features that make it work as inclusion infrastructure

In our work structuring these programmes for African banks and anchors, the same three features explain why the model reaches suppliers that conventional credit cannot.

- The credit decision rides on payment certainty, not borrower credit history. A factoring or reverse-factoring arrangement against a confirmed payable from a creditworthy anchor changes the underwriting model entirely. The supplier does not need a CRB record. The anchor's commitment to pay is what is being financed.

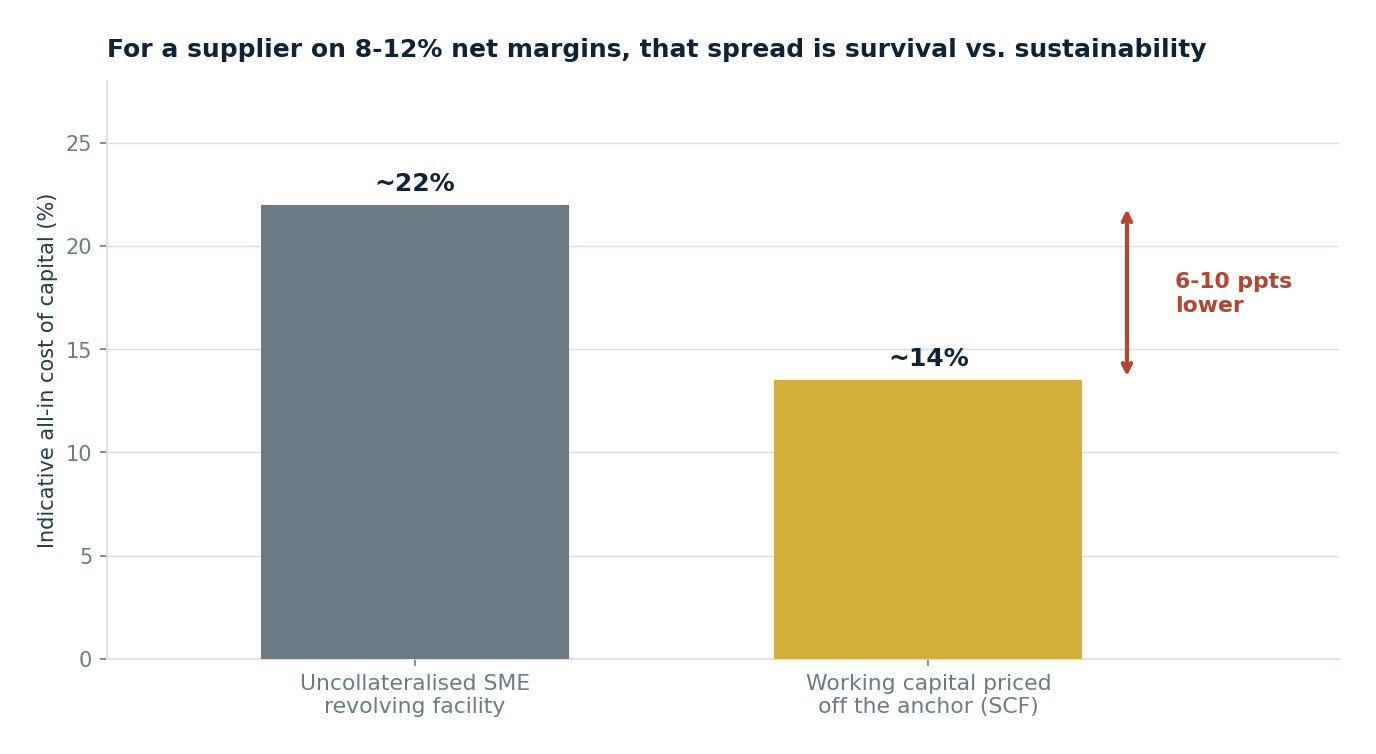

- The cost of capital is materially lower than uncollateralised SME credit. Working capital priced off the anchor's credit profile typically lands at 6 to 10 percentage points lower than equivalent-tenor SME revolving facilities.

- It builds the SME's audit trail. Each invoice that flows through a supply chain finance platform generates verifiable transactional history. After 12 to 18 months on the platform, the supplier has the documented cash-flow record that a Tier 2 bank's SME credit team will accept for an independent working capital facility. The SCF facility becomes the on-ramp.

For a supplier operating on 8 to 12 percent net margins, that 6 to 10 point spread is the difference between a sustainable business and a survival exercise.

What has held the model back in Africa

What has held the model back is not the financial logic. It is the orchestration cost. Onboarding 200 informal suppliers behind one anchor is operationally expensive at low ticket sizes, and most African banks have not built the unit economics to make it work. The technology and orchestration layer required is now mature enough that the constraint is shifting back to the credit appetite question.

Where ARMA comes in

ARMA's supply chain finance build engagement is a 10 to 14 week diagnostic and structuring exercise that delivers an anchor-suitability assessment, a supplier onboarding economic model, a credit policy and pricing framework, and a platform-vendor shortlist - for Tier 1 and Tier 2 African banks, anchor corporates with deep supplier networks, and DFIs structuring supply-chain-finance facilities.