Correspondent banking de-risking: the African bank response

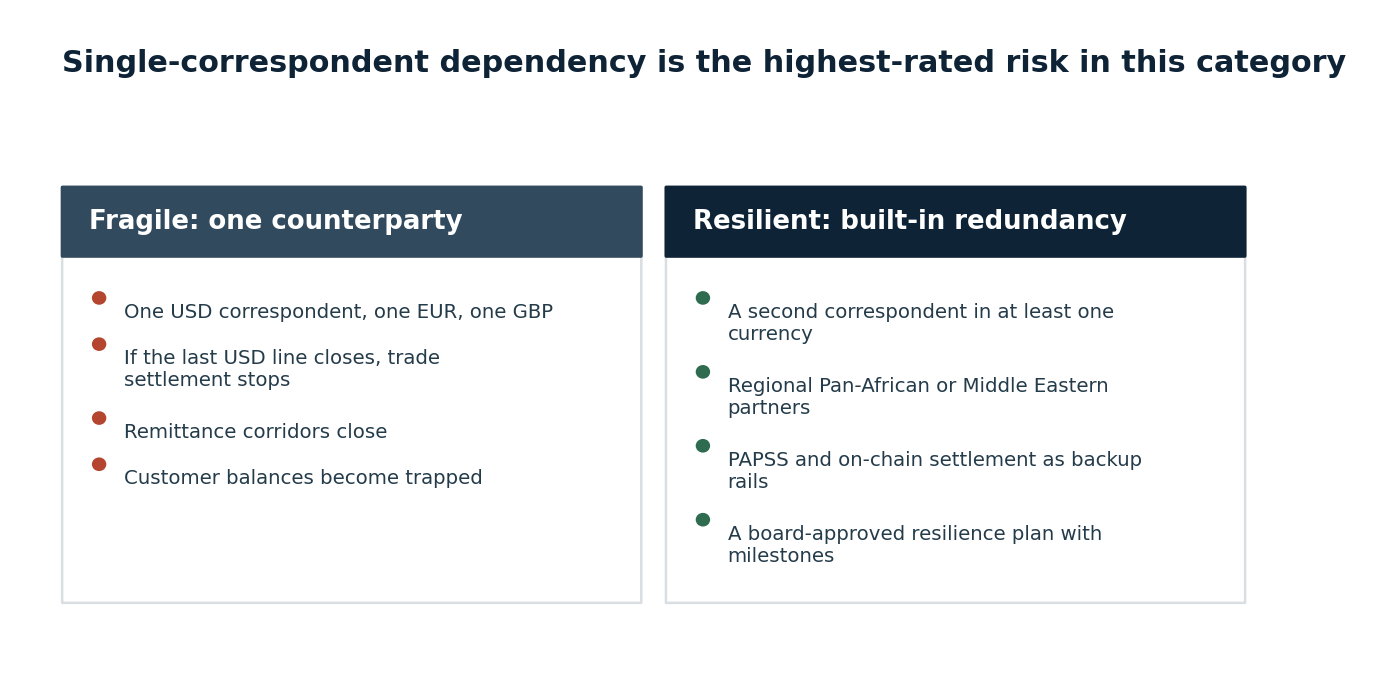

Correspondent banking de-risking is the slow-burn structural threat to African finance that does not get the headlines it should. Global banks have been shedding nostro relationships with African counterparts at a steady rate since 2014, and the 2024 BIS data confirms the trajectory has not reversed. For a Tier 2 or Tier 3 African bank, losing your last USD correspondent is an existential event: trade finance settlement stops, remittance corridors close, and customer balances become trapped.

The risk most banks have not written down

What we observe across African banking clients is consistent: most institutions carry a correspondent banking risk that never makes it onto the enterprise risk register. The treasurer knows the relationship is fragile. The risk officer has not formally documented it. The board has not been asked to approve a contingency plan. The exposure is real, but it is invisible to the people accountable for it.

Three responses, run in parallel

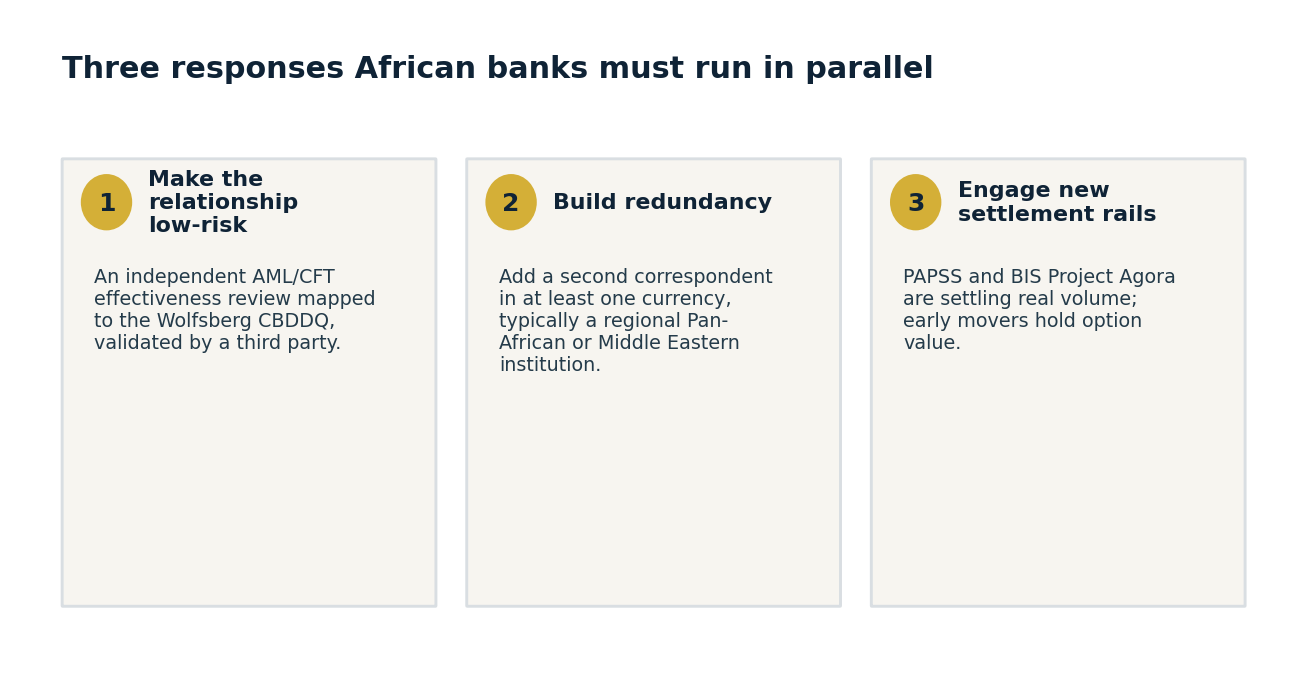

Three responses are realistic, and African banks need to pursue all three at once rather than in sequence.

- Make the relationship demonstrably low-risk. Correspondent banks are not closing relationships because they want to. They close them because the cost of compliance per relationship exceeds the revenue. The single most effective lever is an annual independent AML/CFT effectiveness review delivered in a format that maps directly to the Wolfsberg Correspondent Banking Due Diligence Questionnaire. This is not a CBDDQ submission. It is a third-party-validated capability document that sits behind the CBDDQ and answers the questions the correspondent's compliance team actually asks.

- Build redundancy. Single-correspondent dependency is the highest-rated risk in this category. Most African banks we have worked with have one tier-1 USD correspondent, one EUR, one GBP. A six-month deliberate effort to add a second correspondent in at least one currency, typically a regional Pan-African or Middle Eastern institution, materially reduces tail risk.

- Engage with regional settlement initiatives. PAPSS (the Pan-African Payment and Settlement System) and BIS Project Agora are no longer experimental. They are settling real volume. African banks that move early on these rails hold an option value that banks waiting for them to mature do not.

None of these three is a one-quarter fix. All three need a board-approved correspondent banking resilience plan with measurable milestones.

Where ARMA comes in

ARMA's correspondent banking resilience engagement is an 8 to 12 week diagnostic and capability build that delivers a CBDDQ-mapped independent AML/CFT effectiveness review, a redundancy roadmap with two prioritised target correspondents, and a PAPSS and CBDC readiness assessment. It is built for Tier 2 and Tier 3 African banks where USD or EUR settlement depends on three or fewer counterparties. Visit client.africarisk.net to scope the engagement.