The IFRS S1/S2 implementation gap in African banking

IFRS S1 (general sustainability disclosures) and IFRS S2 (climate-related disclosures) are no longer prospective. They are live standards. Mauritius adopted them in 2024. Nigeria has issued a roadmap. Kenya is consulting. The trajectory is irreversible.

What we are seeing inside African banks tells a different story. Three implementation gaps appear in every IFRS S1/S2 readiness assessment we conduct.

Gap 1: the materiality assessment has never been done

IFRS S1 requires entities to disclose information about sustainability-related risks and opportunities that could reasonably be expected to affect cash flows, access to finance, or cost of capital. Most African banks have a sustainability narrative for marketing purposes. They have not done a board-approved materiality assessment that identifies which sustainability-related risks are financially material to them specifically. The two are not the same thing. The first is a press release. The second is an auditable disclosure baseline.

Gap 2: Scope 3 financed emissions are not measured

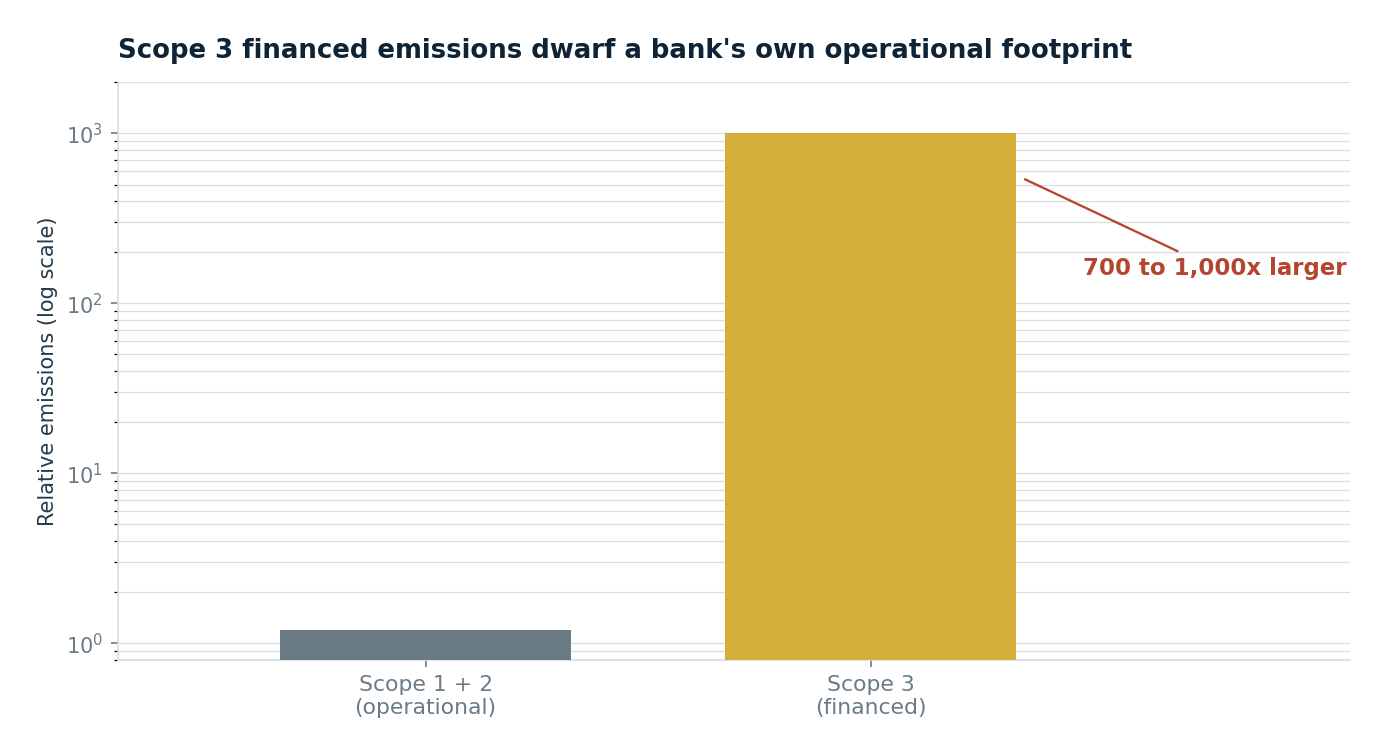

IFRS S2 requires disclosure of Scope 1, 2, and 3 emissions. For banks, Scope 3 financed emissions are typically 700 to 1,000 times larger than operational emissions. African banks generally have a credible Scope 1 and 2 figure: head office electricity, fleet diesel. Scope 3 financed emissions across the loan book is a multi-month measurement exercise using PCAF methodology, requiring portfolio segmentation, emission factor selection, and data quality scoring. Most banks have not started.

Gap 3: climate scenario analysis is treated as a tick-box

IFRS S2 requires entities to use climate-related scenario analysis to assess climate resilience. NGFS scenarios are the standard reference. Many African banks are running shallow physical-risk overlays and calling it scenario analysis. A proper scenario exercise translates a 2 degree or 3 degree pathway into balance-sheet impacts at portfolio level, and most internal teams do not yet have the modelling capacity to do that.

None of these gaps is technically impossible to close. All three require sequenced, multi-quarter work that starts with a board-level materiality assessment and ends with auditor-ready disclosures.

Where ARMA comes in

ARMA's IFRS S1/S2 readiness engagement is a 12 to 16 week diagnostic and capability build that delivers a materiality assessment, a PCAF-aligned financed-emissions baseline for the top three portfolio segments, and a scenario analysis framework your audit committee can sign. It is built for Tier 1 and Tier 2 African banks preparing for their first sustainability-standard audit. Visit client.africarisk.net to scope the engagement.