Why Uganda's July 2026 ESG Risk Framework deadline matters for every East African bank

The Bank of Uganda's ESG Risk Management Framework came into force in mid-2025, and full compliance demonstration is required by July 2026. As of June 2026, most Ugandan and East African banks are treating the deadline as a compliance checkbox. They should be treating it as a capital-access gate.

The framework is not abstract. It requires four concrete capabilities, each of which takes 90 to 180 days of focused work to stand up in an institution that has not built them before. With 13 months elapsed and one month remaining, the institutions that started in Q3 2025 are now in supervisor pre-engagement, those that started in Q1 2026 are in late-stage drafting, and those that have not started are now exposed.

What the framework actually requires

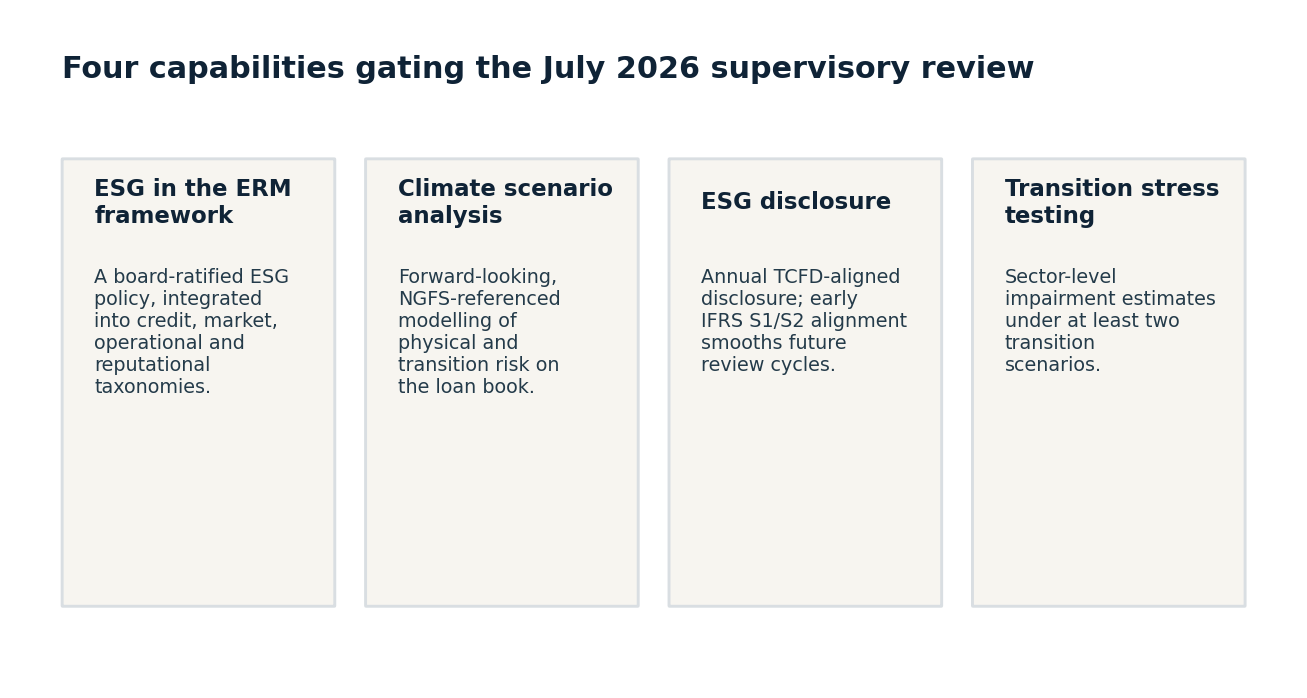

Four capabilities are gating the July 2026 review.

- ESG risk integration into the enterprise risk framework. The framework requires board-level ESG risk oversight, an ESG risk policy ratified at board level, and integration of ESG risk into existing credit, market, operational, and reputational risk taxonomies. The supervisor will ask to see the board minutes, the policy, and the integrated risk register.

- Climate scenario analysis. Banks must demonstrate forward-looking capacity to model climate physical and transition risk on their loan book. NGFS scenarios are the supervisor's expected reference; institutions may use their own scenarios provided the methodology is defensible and the time horizons match supervisor expectations.

- ESG disclosure. Annual ESG disclosure aligned with TCFD principles is required. The framework does not yet mandate IFRS S1/S2 verbatim, but the supervisor has signalled that institutions that align early will face smoother review cycles in 2027 and beyond.

- Stress testing for transition risk. Banks with concentrated exposures to extractive sectors, energy, or transition-vulnerable agriculture must show stress-tested impairment estimates under at least two transition scenarios. Loan-by-loan modelling is not required; sector-level scenario analysis is.

Why correspondent banking exposure compounds the deadline

This is not a Uganda-only issue. Tier-1 commercial banks in Kenya, Tanzania, and Rwanda maintain Ugandan-shilling correspondent relationships through Ugandan partners. If a Ugandan bank fails its July 2026 supervisory review, its correspondent partners face elevated counterparty risk on their UGX positions, and the Kenyan and Tanzanian institutions then face questions from their own supervisors about correspondent exposure to non-compliant institutions.

The ripple is regulatory, not commercial. CBK and BoT are not yet imposing ESG-conditional correspondent rules, but they are watching. The bank that demonstrates ESG capability in 2026 is positioning for correspondent relationship growth in 2027. The bank that does not is positioning for correspondent relationship constraint.

The capability gaps most banks have not closed

In our work with East African institutions through Q1 and Q2 2026, four gap patterns recur.

- Data collection lag. Most banks have not completed a Scope 1, 2, and category-1 Scope 3 financed-emissions inventory. Without baseline data, scenario analysis is impossible. The institutions that started in Q3 2025 have baseline; those that started in 2026 are still mid-collection.

- Modelling capacity. NGFS scenarios are designed for advanced-economy macro. Localising scenarios to East African macro (currency depreciation, drought-cycle agricultural risk, oil-revenue transition for Uganda) requires either an in-house modelling team or external technical assistance. Most banks have neither.

- Governance setup. A board-level ESG committee charter, ratified minutes, and policy text take 60 to 90 days even with focused legal and risk function attention. Many banks have not started this work.

- Disclosure templates. TCFD-aligned templates are not difficult to produce, but they require coordination between risk, finance, and corporate communications. Inter-departmental coordination is the bottleneck most banks underestimate.

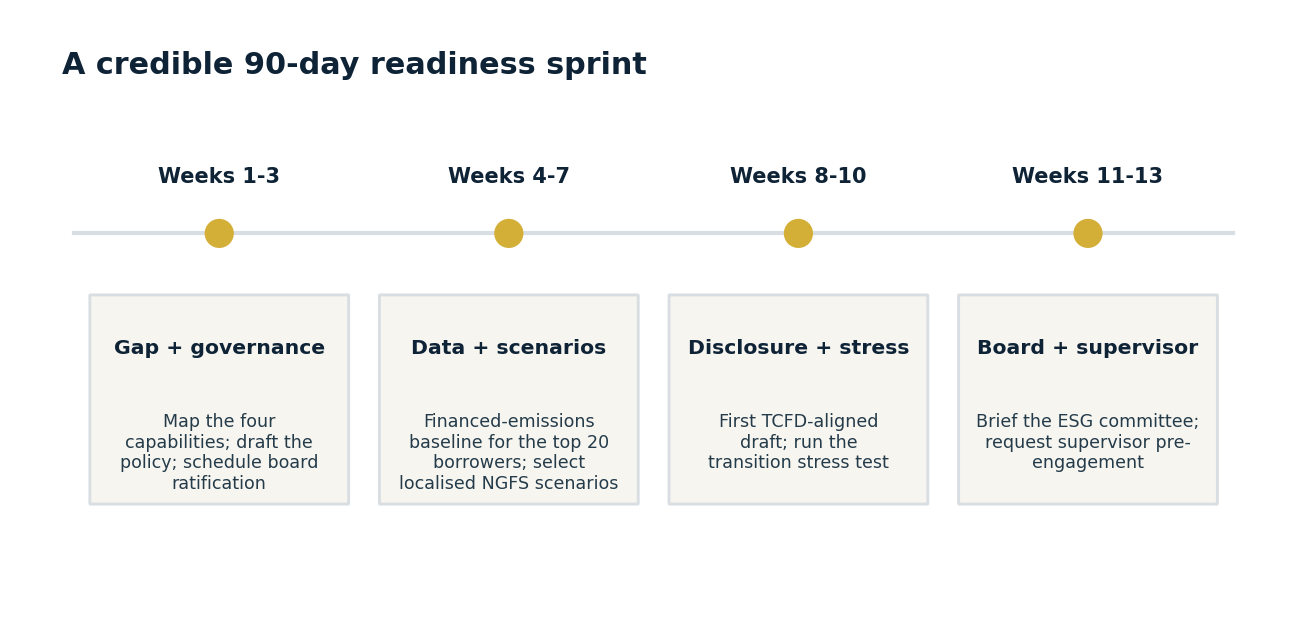

What a credible 90-day readiness sprint looks like

For institutions starting today and aiming to demonstrate credible work-in-progress by the July 2026 supervisory review, even if full compliance lands in Q3 2026, the sequence is achievable.

- Weeks 1 to 3, gap assessment and governance. Map the four required capabilities against current state. Draft the ESG risk policy. Schedule the board ratification. Identify the senior ESG risk owner. The deliverable is a one-page sprint plan signed by the CRO.

- Weeks 4 to 7, data baseline and scenario method selection. Complete the financed-emissions inventory for the top 20 borrowers, which is 80 percent of the exposure for most banks. Select NGFS scenarios localised to your macro. The deliverable is a baseline data set and a scenario methodology memo.

- Weeks 8 to 10, disclosure draft and stress test. Produce the first TCFD-aligned disclosure draft. Run the transition stress test on the selected scenarios. The deliverable is a draft disclosure and a stress test report.

- Weeks 11 to 13, board review and supervisor pre-engagement. Brief the board ESG committee. Request a supervisor pre-engagement meeting. Show your work. The deliverable is a board minute and a supervisor meeting note.

The deadline is not the supervisor's problem. It is yours. The window to address it as a managed sprint, rather than a fire drill, is closing.

Where ARMA comes in

ARMA has supported East African financial institutions on ESG capability standup since the BoU framework consultation phase in 2024. Our delivery model combines AI-augmented baseline modelling (financed-emissions inventories built in days, not weeks), senior practitioner judgement on scenario selection, and direct supervisor pre-engagement support. The complete sprint runs 13 weeks. If your institution is now exposed to the July 2026 deadline and needs to demonstrate credible work-in-progress within 90 days, visit client.africarisk.net to scope the engagement.